You don’t always need a 20% deposit to buying a house in Australia in 2025 – in many cases, you can get into your first home with as little as 5%, and sometimes even 2% or no cash deposit at all with a guarantor. The “right” deposit for you depends on your budget, how quickly you want to buy, and whether you’re eligible for government schemes that reduce or remove Lenders Mortgage Insurance (LMI).

If you’re just starting your journey, a quick House Value Estimator or your target suburbs will show you how much homes are actually selling for, so you can see exactly how much you need to save. From there, you can compare what a 5%, 10% or 20% deposit looks like in real dollars, and decide whether it’s smarter to buy sooner with a smaller deposit or wait longer and aim for the traditional 20%.

Understanding Your Deposit Options

When it comes to buying a house, your deposit amount directly impacts everything from your loan approval to your monthly repayments. Here’s what different deposit levels mean for you in 2025.

The 20% Deposit: The Traditional Route

A 20% deposit remains the ideal benchmark for most lenders. This means borrowing just 80% of the property’s value, keeping your loan-to-value ratio (LVR) low. The major advantage here is avoiding Lenders Mortgage Insurance (LMI), which can save you thousands of dollars.

For example, if you’re eyeing a property worth $600,000, you’d need to save $120,000 for a 20% deposit. This gives you access to better interest rates and more favourable loan terms. However, with median house prices across Australia reaching $844,000, saving this amount can take anywhere from six to ten years, depending on your location and income. Using a Property Price Estimate tool before you commit to a savings goal can give you a clearer picture of how realistic a 20% deposit is for your preferred area.

The 10% Deposit: Meeting Halfway

Can’t quite reach that 20% mark? A 10% deposit is still a solid option. On that same $600,000 property, you’d need $60,000 saved. You’ll likely pay LMI, which typically adds between $8,000 and $12,000 to your loan costs at this deposit level, but it gets you into the market years sooner.

Many first-time buyers find that this sweet spot allows them to enter the property market while prices are still within reach, rather than watching values climb while they continue saving.

The 5% Deposit: Your Fast Track to Homeownership

Here’s where buying house in Australia becomes truly accessible for first-time buyers. Thanks to the expanded First Home Guarantee scheme launched in October 2025, eligible buyers can now purchase with just 5% deposit without paying LMI.

This game-changing initiative removed all income caps and placed limits, while increasing property price caps to align with average house prices across different regions. For a $600,000 home, you’d only need $30,000 saved instead of $120,000. That’s potentially six to ten years shaved off your savings timeline.

First home buyers using this scheme are expected to save around $1.5 billion in LMI costs in the first year alone. For someone buying an affordable home under $650k in regional areas, this makes homeownership significantly more achievable.

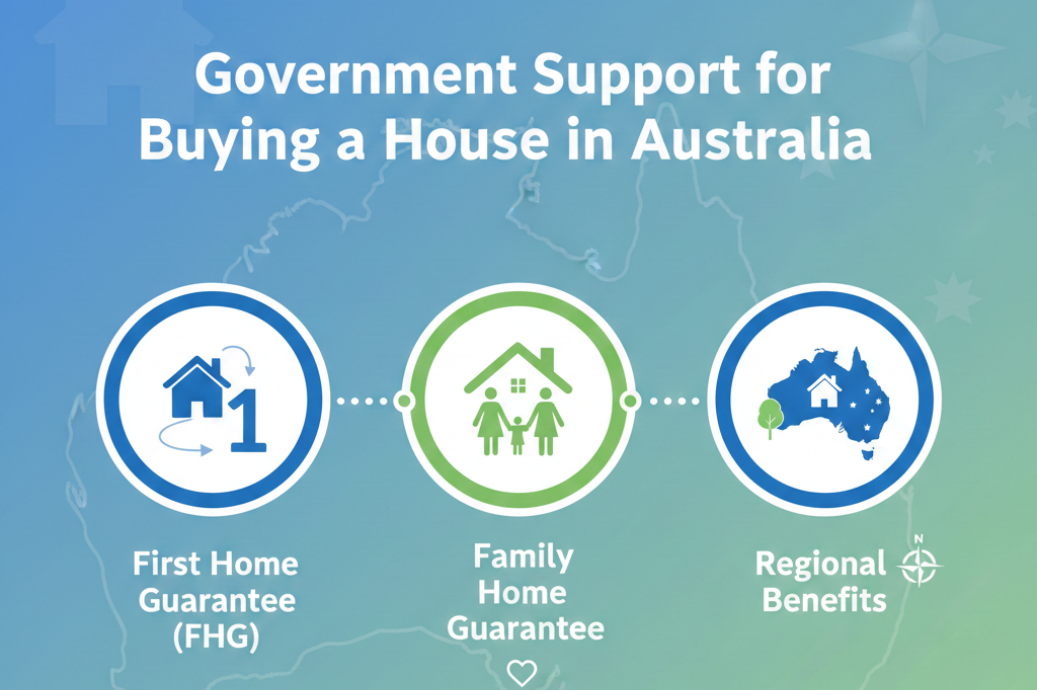

Government Support That Makes a Difference

The Australian government has introduced several schemes specifically designed to help buyers enter the market with smaller deposits:

First Home Guarantee (FHG): Available to all first-home buyers from October 1, 2025, this allows you to purchase with just 5% deposit. Housing Australia guarantees up to 15% of the property’s value, eliminating the need for LMI. Property price caps vary by location, with Brisbane buyers able to purchase homes up to $1 million.

Family Home Guarantee: Single parents or guardians can buy with as little as 2% deposit. This scheme offers 5,000 places annually for eligible applicants.

Regional Benefits: If you’re buying a house in NSW regional areas, you may find even more affordable options combined with these government schemes.

What About Lenders Mortgage Insurance?

Understanding LMI is crucial when buying house with less than 20% deposit. This insurance protects the lender (not you) if you default on your loan. While it adds to your upfront costs, it shouldn’t necessarily stop you from purchasing.

For a $500,000 loan with different deposits, here’s what you might pay:

- 10% deposit: LMI approximately $8,000-$12,000

- 5% deposit: LMI approximately $15,000-$20,000

The key is weighing LMI costs against potential property price growth. If prices increase by 5% annually, waiting another two years to save a larger deposit could mean the property costs $60,000 more. In this scenario, paying $15,000 in LMI actually saves you money.

Affordable Options Still Exist

While major cities like Sydney and Melbourne have median prices well over $1 million, plenty of cheap houses for sale exist throughout Australia. Regional areas particularly offer excellent value.

Looking for Australia cheap home sale opportunities? Areas like Greater Western Sydney, Moreton Bay region near Brisbane, and Adelaide’s middle ring still offer homes under $650,000. Coastal areas like those near Jervis Bay Real Estate markets provide lifestyle properties at more reasonable price points than major metropolitan centres.

Even Brisbane, experiencing strong growth predictions of 9–14% for 2025, has hidden gem suburbs where affordable homes under $650k remain available for savvy buyers willing to look beyond the CBD. A good local agent can explain how Real Estate Agent Payment works and structure an agreement that aligns with your budget and selling or buying strategy.

Beyond the Deposit: Additional Costs to Budget For

Remember, your deposit isn’t the only upfront cost when buying a house. Factor in these essential expenses:

Stamp Duty: This government tax varies by state and property price. First-home buyers often qualify for exemptions or discounts.

Legal Fees: Conveyancing and legal services typically cost $1,500-$3,000.

Building Inspection: Essential for protecting your investment, expect to pay $400-$800.

Loan Application Fees: Some lenders charge setup fees, though many now waive these.

Smart Strategies to Reach Your Deposit Goal

Getting to your deposit target faster requires discipline and smart planning:

Set a Clear Target: Calculate exactly what you need and work backwards to determine monthly savings.

Automate Your Savings: Transfer money to a high-interest savings account immediately after payday. Treating savings as a non-negotiable expense works.

Reduce Major Expenses: Consider cheaper accommodation or finding a roommate temporarily. Two years of reduced rent can make an enormous difference.

Clear Existing Debts: Credit card balances and personal loans reduce your borrowing power. Tackle these first.

Generate Extra Income: Side gigs, overtime, or freelance work directed entirely to savings can accelerate your timeline significantly.

Explore First Home Owner Grants: State-based grants can provide $10,000-$30,000 toward your purchase, varying by location and property type.

Guarantor Loans: The 0% Deposit Option

Some buyers explore guarantor loans, where a family member (typically parents) uses their property equity as security for your loan. This can allow you to purchase with no deposit saved and potentially avoid LMI.

While this fast-tracks homeownership, it’s a serious decision. The guarantor’s property is at risk if you can’t meet repayments, and it affects their borrowing capacity. Professional financial advice is essential before pursuing this path.

Making Your Decision

The right deposit amount depends on your personal circumstances, financial position, and property goals. While 20% remains ideal for the best loan terms, don’t let it become a barrier to homeownership.

For many buyers in 2025, the 5% deposit option through the First Home Guarantee provides the perfect balance—getting into the market sooner while avoiding excessive LMI costs. This is particularly true in markets where property prices continue rising faster than you can save.

The reality of buying a house in Australia today means being strategic and realistic. Research your target suburbs, understand all available schemes, and calculate the true cost of waiting versus buying with a smaller deposit.

Ready to Start Your Homeownership Journey?

At Wright Way Realty, we understand that navigating deposits, government schemes, and the current property market can feel overwhelming. Whether you’re exploring cheap houses for sale in regional areas or searching for your perfect property in competitive markets, we’re here to guide you through every step.

Our experienced team knows the local market inside and out and can help you identify opportunities that align with your budget and goals. Don’t let deposit requirements hold you back from achieving your dream of homeownership.

Contact Wright Way Realty today to discuss your property goals and discover how we can help you find the right home at the right price. Your journey to homeownership starts with taking that first step—and we’re here to walk alongside you every step of the way.